All Categories

Featured

Table of Contents

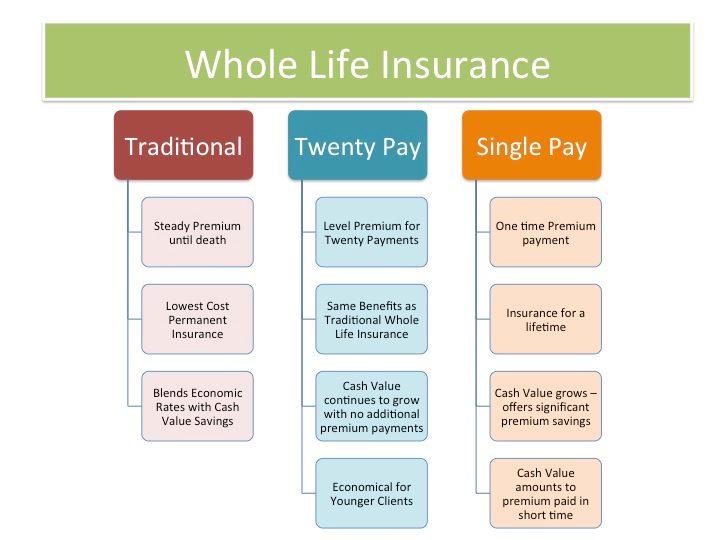

A PUAR enables you to "overfund" your insurance plan right approximately line of it ending up being a Customized Endowment Contract (MEC). When you use a PUAR, you rapidly boost your money value (and your survivor benefit), therefore increasing the power of your "bank". Further, the more money value you have, the better your rate of interest and returns settlements from your insurance coverage company will be.

With the surge of TikTok as an information-sharing platform, financial recommendations and techniques have actually found a novel means of dispersing. One such technique that has been making the rounds is the unlimited banking principle, or IBC for brief, gathering endorsements from celebs like rapper Waka Flocka Fire. While the approach is presently preferred, its roots map back to the 1980s when economic expert Nelson Nash presented it to the world.

What are the benefits of using Bank On Yourself for personal financing?

Within these plans, the cash money worth expands based upon a price set by the insurer (Infinite Banking wealth strategy). Once a significant cash money value builds up, insurance holders can obtain a money worth financing. These finances vary from standard ones, with life insurance policy working as collateral, implying one might lose their protection if borrowing exceedingly without sufficient money value to sustain the insurance expenses

And while the attraction of these policies appears, there are natural restrictions and risks, necessitating persistent money value monitoring. The technique's authenticity isn't black and white. For high-net-worth individuals or service owners, specifically those using methods like company-owned life insurance policy (COLI), the benefits of tax breaks and substance growth can be appealing.

The allure of infinite financial does not negate its challenges: Price: The foundational requirement, an irreversible life insurance policy policy, is more expensive than its term counterparts. Qualification: Not everybody gets approved for entire life insurance policy because of extensive underwriting procedures that can exclude those with certain health and wellness or way of life conditions. Intricacy and risk: The complex nature of IBC, combined with its dangers, may hinder many, specifically when less complex and much less high-risk alternatives are readily available.

Self-banking System

Alloting around 10% of your regular monthly revenue to the policy is just not practical for a lot of individuals. Part of what you review below is simply a reiteration of what has already been stated over.

Prior to you obtain yourself into a scenario you're not prepared for, know the following first: Although the concept is typically offered as such, you're not actually taking a finance from on your own. If that held true, you wouldn't need to repay it. Instead, you're borrowing from the insurer and need to settle it with rate of interest.

Some social networks blog posts suggest utilizing money worth from entire life insurance policy to pay for credit history card financial debt. The concept is that when you repay the loan with rate of interest, the quantity will be sent out back to your investments. Unfortunately, that's not exactly how it works. When you pay back the finance, a portion of that rate of interest goes to the insurance coverage company.

For the very first several years, you'll be paying off the commission. This makes it incredibly tough for your policy to accumulate worth during this time. Unless you can afford to pay a few to several hundred bucks for the next decade or even more, IBC will not function for you.

How do I qualify for Leverage Life Insurance?

Not everyone must depend solely on themselves for monetary safety and security. If you need life insurance policy, right here are some valuable ideas to think about: Consider term life insurance coverage. These policies supply protection throughout years with substantial economic commitments, like home loans, trainee finances, or when looking after young youngsters. Make certain to go shopping around for the very best price.

Envision never ever needing to worry about small business loan or high passion rates once more. Suppose you could obtain cash on your terms and build wealth all at once? That's the power of unlimited banking life insurance coverage. By leveraging the money worth of entire life insurance IUL plans, you can expand your wide range and borrow money without depending on traditional banks.

There's no set finance term, and you have the flexibility to choose the repayment routine, which can be as leisurely as settling the finance at the time of fatality. Infinite Banking for financial freedom. This adaptability encompasses the servicing of the loans, where you can choose interest-only payments, keeping the car loan equilibrium flat and workable

Holding cash in an IUL dealt with account being credited interest can frequently be better than holding the money on deposit at a bank.: You've always dreamed of opening your very own bakery. You can borrow from your IUL plan to cover the preliminary expenses of leasing a space, buying tools, and hiring staff.

Cash Value Leveraging

Personal loans can be acquired from conventional banks and lending institution. Here are some key points to consider. Charge card can give an adaptable way to obtain money for very short-term periods. However, obtaining money on a credit report card is generally really costly with interest rate of passion (APR) commonly getting to 20% to 30% or more a year - Infinite Banking.

{kind=link}

Latest Posts

Life Without The Bank & Becoming Your Own Banker

Unlocking Wealth: Can You Use Life Insurance As A Bank?

Be Your Own Bank: 3 Secrets Every Saver Needs